AIG could hardly support its pre-bailout debt, let alone an additional $115 billion of debt and dividend-bearing preferred stock. For AIG’s balance sheet to be healthy again, leverage needs to come down by approximately $150 billion. It appears unlikely that this can be achieved through asset sales. AIG needs more immediate attention, and the company’s franchise value erodes each day that a permanent fix is delayed.

The original “bailout” consisted of an $85 billion credit facility with the NY Fed, in connection with which a trust for the U.S. Treasury purchased a 79.9% equity stake in AIG for $0.5 million. The deal has since been revised and now totals approximately $168 billion, comprised of:

- $115 billion provided directly to AIG, including:

- The Fed credit facility, which was reduced to $60 billion;

- $40 billion of preferred stock; and

- Access to the NY Fed commercial paper program, through which $15.2 billion had been borrowed as of November 5th; and

- $52.5 billion of off-balance sheet loans, including:

- $22.5 billion to facilitate the termination of AIG’s securities lending program, and

- $30 billion to facilitate the termination of certain CDS contracts. 1

The analysis below shows that AIG’s balance sheet was over-leveraged before the bailout, so the additional debt and preferred stock just compounds the problem. The leverage piled onto AIG’s balance sheet, primarily to satisfy parties to its CDS and securities lending agreements, needs to be restructured again.

Windfall for CDS Counterparties and CDO Holders

AIG’s liquidity crisis became critical when rating agencies lowered AIG’s ratings by several notches last September, which triggered collateral calls on certain CDS contracts. If AIG did not post required collateral, counterparties to the CDS agreements could terminate them, requiring AIG to come up with the full “notional”2 amount of the CDSs. Termination payments would have been nearly twice as large as the collateral requirements. The Fed credit facility enabled AIG to meet its collateral calls and avoid terminations. Through November 5th, AIG had posted or agreed to post collateral totaling $39.9 billion with respect to credit default swaps.

The problems stemmed primarily from the unique terms of a small segment of AIG’s CDS portfolio with a notional amount of $71.6 billion or 19% of the $377.3 billion total CDS portfolio as of 9/30/08. This segment, CDS agreements written on the “super senior”3 tranches of multi-sector CDOs, is unique in that the “exposure” on these agreements is not calculated using default models. Instead, it is based on the market value of the underlying securities. This feature greatly magnified the volatility and mark-to-market losses for these CDSs.4

click to enlarge

Prices of the underlying securities5 suddenly plummeted after the initial Fed/Treasury deal, as market spreads shot up, so something more had to be done. With the revised Fed/Treasury deal came a plan to terminate the “super senior” CDS contracts after all, and purchase the underlying CDOs. Of the $52.5 billion in off-balance sheet financing referenced above, $30 billion is a loan to Maiden Lane III LLC (ML III), an entity formed by the NY Fed and AIG to purchase (at market value) $64.7 billion face value of the “super senior” CDO tranches on which AIG had written CDS agreements (AIG invested $5 billion in ML III). In connection with the purchase of the CDOs, the related CDS agreements are being terminated.6

This is a huge windfall for the holders of these CDOs,7 which go from owning extremely illiquid securities carried on their balance sheets at pennies on the dollar, to getting cashed out at or near par (through the combination of the market purchase of the CDOs and the CDS collateral and termination payments). Prior to the initial Fed/Treasury bailout, these parties could have threatened to put AIG into bankruptcy if AIG did not post the required additional collateral, but in reality their negotiating leverage was limited. The collateral they held was only a fraction of the amount owed to them if the CDS agreements were terminated, and their unique status in bankruptcy as parties to “financial transactions” only gave them the ability to keep the collateral they had. Their additional claims would likely have been treated like any other prepetition unsecured claims.8 Despite their questionable seniority, they are being made whole.

There are probably some senior secured creditors of AIG that wish they got the same deal….

The $150 Billion Problem

While it is difficult to calculate precisely how much debt AIG’s operations can support, the analysis below provides an approximation.

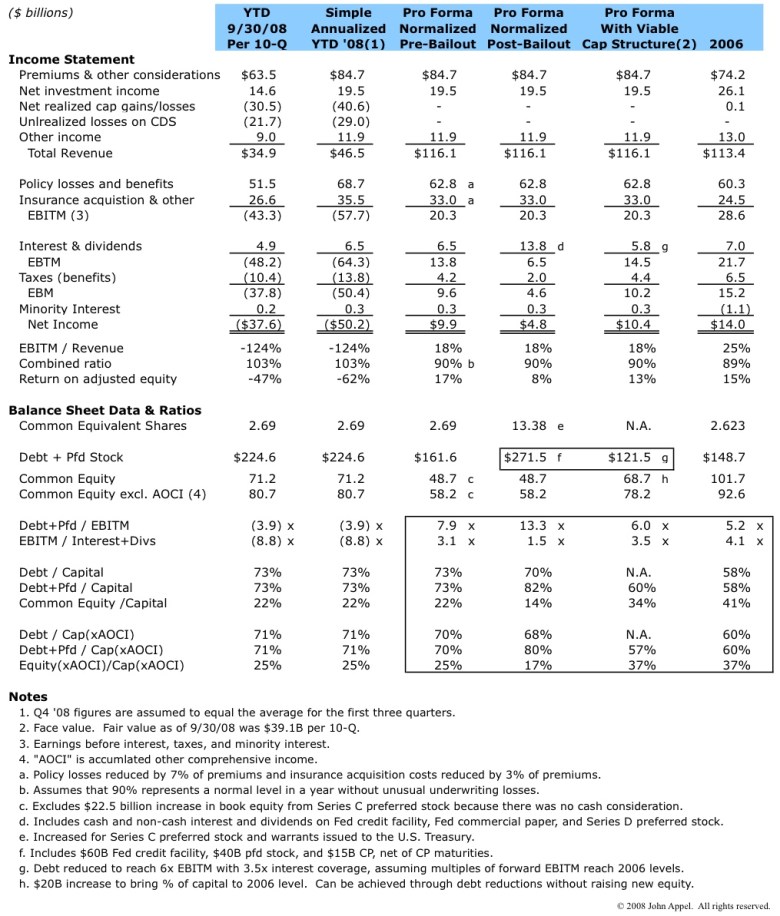

One can get a sense of AIG’s potential normalized revenue and operating profits, and the debt that can be supported by those profits, by going back to 2006, when the performance of AIG’s Financial Products group had little impact on the business. Below is a summary of relevant 2006 financial data.

The table shows that 2006 was a banner year for AIG. With low losses and high investment returns, earnings before interest, taxes and minority interest (EBITM) was 25% of revenue, and the company had a 15% return on adjusted equity. Debt amounted to about 5x EBITM and interest coverage (EBITM/Interest) was about 4x. Presumably this was the type of leverage multiple and interest coverage that was necessary to maintain its ratings.

The table below compares 2008 to 2006. For 2008, the table shows actual results for the year-to-date ended 9/30/08, annualized YTD 2008 results, and pro forma normalized results with and without the bailout. One can see in the third column that AIG was over-leveraged before the bailout, with debt of nearly 8x normalized EBITM. More debt and preferred stock was the last thing AIG needed. The bailout leaves AIG leveraged at over 13x normalized EBITM, with interest coverage of only 1.5x. To bring its leverage and capital ratios back to 2006 levels, it appears that AIG needs to reduce its debt and preferred stock by $150 billion (the difference between what is shown in the fourth and fifth columns).

click to enlarge

Asset Sales – Too Little Too Late

AIG and the architects of the bailout knew that the structure was not a permanent fix, but anticipated that sufficient assets could be sold to repay the U.S. government funding and achieve the deleveraging needed to stabilize the balance sheet. The main assets identified for sale are the aircraft leasing business (ILFC) and the life insurance operations. I estimate the book value of ILFC at approximately $10 billion.9 With approximately $1 billion in operating income, ILFC would probably sell for about 1x book value in a normal economic environment, but in the current environment, I would not be surprised if the number is half this amount. I estimate the unlevered book value of the Life Insurance and Retirement Services business at roughly $135 billion.10 Given that operating income for this segment is in the range of $8-10 billion, it is hard to imagine even the most strategic buyers paying 1x book. A more realistic figure today might be closer to $80 billion (about 1.5x revenue and a high single-digit multiple of operating income).

Whether these assets are sold in the near term, for proceeds perhaps in the range of $80-90 billion, or a few years from now for something closer to $150 billion, it will not be enough to fix AIG’s balance sheet. While debt would be reduced, operating cash flow to service debt would be reduced as well, so the remaining business would still be over-leveraged.

One Potential Solution

AIG attempted to raise capital in the private sector, enlisting the help of Blackstone, J.P. Morgan, and Goldman Sachs. The company spoke to private equity funds, sovereign wealth funds and other potential investors. J.P. Morgan and Goldman tried to syndicate a $75 billion lending facility – but all of these attempts failed. AIG summarizes this whole saga here.

Given the state of AIG’s balance sheet, the unknown (and perhaps unknowable) risks in its investment portfolio, litigation risks from disgruntled shareholders and others, and many other factors, it is likely that the private sector would have required AIG to reorganize through Chapter 11. The company’s total obligations were just too big to be met from present or foreseeable cash flows of the business.

If it is in the best interest of the global financial system for AIG not to go through Chapter 11, then the U.S. government should help engineer an alternate way to remediate AIG’s balance sheet permanently, not just plug a short-term liquidity gap by adding even more debt and dividend-bearing preferred stock.

There are many ways in which AIG and the U.S. government could address this. One possible approach would be:

- The Fed or Treasury purchase AIG’s investment in ML III for $42 billion in debt reduction (the Fed and/or Treasury would then own the “super senior” CDOs at par);

- Instead of the Fed lending $22.5 billion to Maiden Lane II to buy RMBS securities from AIG (in connection with the wind-down of AIG’s securities lending program), the Fed buy the securities from AIG for $22.5 billion in cash plus $17.5 billion of debt reduction (the Fed and/or Treasury would then own the RMBS at par);

- The Treasury exchange its Series D Preferred Stock for a new series of convertible preferred stock that converts at a price based on the price of the common stock at some future date, and sell its Series C Preferred Stock and warrants back to AIG at cost; and

- AIG sell (at net book value) businesses with expected net asset values of over $50 billion to an entity jointly owned by AIG and the NY Fed or Treasury in return for a cash payment to AIG of $50 billion.

The sum of these actions would reduce AIG’s net debt and dividend-bearing preferred stock by an aggregate of $150 billion; increase book equity by perhaps $30 billion; and enable the complete pay-down and termination of the Fed credit facility. AIG would have a healthy balance sheet immediately and could refocus on building its businesses and shareholder value. Taxpayers would ultimately be paid back through the CDO and RMBS pools, the orderly sale of business assets, and the eventual conversion and sale of the new preferred stock.

There are many other approaches one could use to achieve similar results, but one way or another, the current Fed/Treasury deals need to be restructured.

(Disclosure: The author does not own any interests in American International Group, except indirectly as a United States taxpayer.)

Footnotes:

1 Below is a more detailed summary of the revised agreements with the Fed and Treasury. For an even more complete description, please see footnote 11 to AIG’s Q3 financial statements (“Subsequent Events” – beginning on page 43).

- Certain AIG subsidiaries entered into a securities lending agreement with the NY Fed, through which the NY Fed provided liquidity to AIG by borrowing, and posting cash collateral for, $19.9 billion of securities. Since then, AIG and the NY Fed have formed a special purpose entity, Maiden Lane II LLC, to buy $40 billion face amount of RMBS from AIG subsidiaries for $23.5 billion in connection with the termination of AIG’s U.S. securities lending operations. The NY Fed will be repaid the $19.9 billion of collateral with a portion of the proceeds.

- The NY Fed agreed to lend up to $30 billion to a special purpose entity, Maiden Lane III LLC, formed to purchase (on market terms) the CDOs underlying most of the credit default swaps written on “super senior” multi-sector CDOs.

- Affiliates of AIG were given access to the NY Fed commercial paper program, through which $15.2 billion had been borrowed as of November 5th to enable AIG to pay down borrowings under the Fed credit facility to $61 billion from $77 billion.

- The U.S. Treasury invested $40 billion in Series D preferred stock with a 10% dividend rate.

- The U.S. Treasury was given warrants for 2% of AIG’s common equity.

- Terms of the Series C convertible preferred stock provided to the Treasury in connection with the Fed credit facility were modified so that it is convertible into 77.9% of the common shares instead of 79.9%.

- The Fed credit facility was reduced from $85 billion to $60 billion, and the interest rate was reduced to LIBOR plus 3%.

2The “notional amount” is the face amount of reference securities on which the credit default swap is written.

3The super senior tranche is one that is not exposed to default risk until the less senior tranches, including the AAA-rated slice just below the super senior slice, have been wiped out. As of 9/30/08, multi-sector CDOs on which AIGFP wrote protection on the super senior tranche had a gross notional amount of $108.5 billion, of which the super senior tranche was $71.6 billion, with the difference being the subordinated layers that would need to be exhausted before the super senior tranche would experience a loss. Below is a graphical representation from AIG’s Q3 10-Q:

4 Most of these agreements also require physical settlement, meaning that instead of a cash settlement equal to the difference between the notional amount of the CDS and the “exposure” on the settlement date, the agreements require AIG to deliver the full notional amount of the CDS in return for delivery of the underlying securities.

5 The multi-sector CDOs were comprised of prime RMBS (11.3%), Alt-A RMBS (15.8%), subprime RMBS (37.1%), CMBS (21.5%), CDOs (9.4%), and other (4.9%) [Note: CDO percentage corrected 1-6-09].

6 As of November 25th, $46.1 billion of CDOs had been purchased and a corresponding notional amount of CDS agreements terminated, with the remaining $18.6 billion in process (See Form 8-K for more details).

7These CDO/CDS holders include Société Générale, Goldman Sachs, Deutsche Bank, Crédit Agricole, and Merrill Lynch (Source: WSJ).

8 Changes to the Bankruptcy Code in 2005 and 2006 expanded the rights of CDS counterparties in a bankruptcy, but the main effect was to enable these parties to enforce termination provisions and collect collateral. Any claims not satisfied by the collateral are still treated as prepetition claims (11 U.S.C. § 502(g)(2)).

9 $45 billion of identifiable assets as of 9/30/08 less $35 billion of ILFC debt leaves $10 billion of net assets. There are probably other operating liabilities of ILFC, so the actual book value is likely to be lower.

10 Identifiable assets of $615 billion as of 12/31/07 per 10-K, less $30 billion change in invested assets as of 9/30/08, less $450 billion reserves, contract deposits, DAC/VOBA & SIA leaves $135 billion of net assets excluding debt. As with ILFC, the actual book value is likely to be lower.

| Copyright © 2008-2009 by John G. Appel. All rights reserved. You may link to any Content on this website. You may not republish, upload, post, transmit or distribute any Content without prior written permission. If you are interested in reprinting, republishing or distributing Content, please contact John Appel via the e-mail address shown on this website to obtain written consent. Modification of Content or use of Content for any purpose other than your own personal, noncommercial use is a violation of our copyright and other proprietary rights, and can subject you to legal liability. Disclaimer: This website is provided for informational purposes only. Nothing on this website is intended to provide personally tailored advice concerning the nature, potential, value or suitability of any particular security, portfolio or securities, transaction, investment strategy or other matter. You are solely responsible for any investment decisions that you make. Terms of Use: By using the site, you agree to abide by the Terms of Use, which includes further copyright information and disclaimers. |

| www.aptacapital.com | John Appel |