The latest installment of the American International Group (AIG) “Bailout” is not the good news that one might imagine from reading AIG’s press release. It does not provide as much financing as originally anticipated. More importantly, it is a reminder that, so far, the U.S. government has done much more to minimize losses for AIG’s counterparties than to maximize value for AIG.

AIG and the Federal Reserve Bank of New York announced on Tuesday that Maiden Lane II, an entity owned and controlled by the NY Fed, has purchased nearly $40 billion of mortgage-backed securities (RMBS) from AIG subsidiaries. This was part of the revised U.S. government bailout announced on November 10th. I described these arrangements in my article last week entitled, “AIG’s Bailout Needs a Bailout: A $150 Billion Problem.”

Edward M. Liddy, AIG Chairman and Chief Executive Officer, said: “AIG’s highest priority is the full repayment of the federal loan facility with interest. The creation and launch of this financing entity will eliminate the liquidity issues associated with AIG’s U.S. securities lending program, which will facilitate our repayment plan. Although we have more work ahead of us, this is an important step forward. We appreciate the support of the Federal Reserve Bank of New York in implementing this transaction.” This seems to imply that this ‘financing entity’ is a new development that frees up AIG capital that otherwise would have gone to satisfy securities lending payables.

While the transaction is a means of financing AIG’s securities lending payables, it is part of the bailout plan and does not provide any capital beyond that anticipated in the bailout. In fact, it provides somewhat less. The illustration in AIG’s November 10th 10-Q1 filing shows a purchase price of $23.5 billion, based on fair market values on September 30th. The actual transaction was based on lower values as of October 31st, and the purchase price was $19.8 billion instead of $23.5 billion.

In my previous analysis, I assumed, based on the 10-Q disclosure, that $23.5 billion would cover substantially all of the securities lending payables, and the financing would provide $22.5 billion, leaving $1 billion to be paid by AIG. In the final deal, these payables required $24.9 billion – the $19.8 billion of sale proceeds plus a $5.1 billion capital contribution from AIG. In other words, the final deal required an additional $4.1 billion from AIG.

The real bad news here is not that the value of these RMBS securities fell by $3.7 billion, or 15.7%, in one month; nor is it that AIG had to contribute $4.1 billion more to wind down its securities lending business. The bad news is that until the deal was finalized, the NY Fed had the ability to make it a more effective tool for saving AIG, and now that chance is gone.

The NY Fed has purchased a portfolio of mortgage-backed securities for 50 cents on the dollar. This price is more reflective of the lack of liquidity in the market than default rates. It is likely that a price of around 80% of par would have more closely approximated the ultimate recovery if the securities were held to maturity.2 The NY Fed’s agreement to share a small portion3 of the gains with AIG after its loan to Maiden Lane II is repaid does little to help things today. This should turn out to be a nice investment for taxpayers.

While some of the legal details have yet to be ironed out, it is clear that the U.S. government controls AIG. The U.S. government can choose to maximize the long-term value of AIG’s most important assets – its reputation and its people – or it can focus on the salvage value of its financial assets. Its actions to date indicate that it is focused more on the latter than the former.

So far, the U.S. government has made sure that banks, investment banks and other parties to AIG’s credit default swaps and securities lending agreements are made whole, even though these parties do not have the most senior rights as creditors. Now that a partial list of the beneficiaries of these transactions has been made public, it is becoming clear that if these institutions had been forced to bear some loss as part of a negotiated deal outside of bankruptcy, the financial system would not have buckled. The U.S. government made a policy decision to help certain members of the financial system that had transacted business with AIG, and has handed the bill to AIG. Whether or not the policy decison is justified, forcing AIG to bear the entire cost is not.

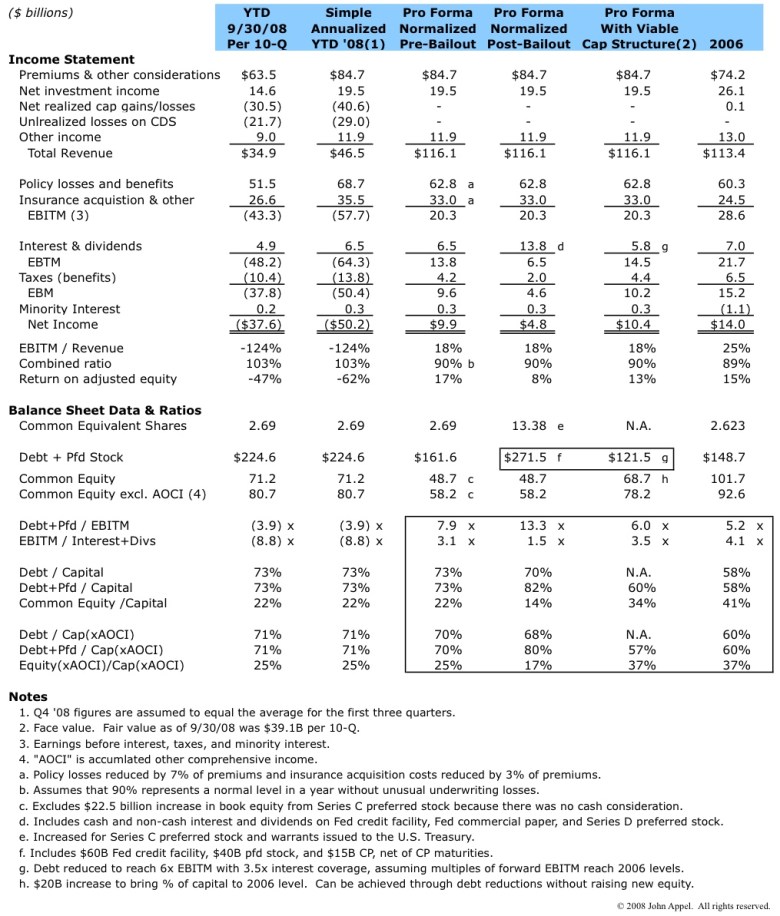

Nearly all of the $170+ billion bailout has gone to fund losses on securities that are no longer on AIG’s balance sheet and have nothing to do with AIG’s go-forward business, so nearly all of the bailout funding arguably should have been funded off-balance sheet. Instead, only about $50 billion is being funded off-balance sheet through Maiden Lanes II and III.

As a result, AIG is saddled with over $270 billion of debt and high dividend preferred stock, compared to under $150 billion in 2006. As I explained in my analysis last week, the $270 billion needs to come down to around $120 billion before AIG’s balance sheet will truly be stabilized, and deserving of its ratings. The plan is to achieve this through asset sales, but this is fallacy. The current value of the assets targeted for sale is probably less than half of the amount needed. Besides, the operating income from the targeted businesses4 may represent nearly half of AIG’s total normalized operating income, so if they were sold, the amount of debt that the remaining businesses could support would be far less than $120 billion.

AIG can limp along on “life support” for several years, since interest and dividends on $100 billion of the financing can just accrue instead of being paid in cash, but this just adds to the bill down the road.

The industry and AIG’s employees know that AIG’s current situation is not sustainable, and it is starting to show. AIG disclosed in its 10-Q that its business is being negatively impacted by its financial instability. And the company’s loss of senior executive Kevin Kelly to a competitor last week is just one example of what will happen to AIG’s executive ranks if things are not stabilized soon.

It is not clear if the U.S. Government cares about this, or if the intent is to break up the business, run-off the assets, and hope to recover at least the debt portion of the bailout funds. It is not too late to choose the growth strategy over the wind-down strategy, but if growth is indeed the goal, the current course must change quickly.

Footnotes:

1 Please see the “Subsequent Events” section of AIG’s Q3 form 10-Q filed on November 10, 2008 (page 45).

2 As of September 30th, AIG’s RMBS included $14 billion each of Alt-A and subprime loans (the bulk of the rest was Agency and Prime). In October, 18.2% of all U.S. subprime loans were in foreclosure or REO, and another 10.4% were 90+ days past due (download data). Of all Alt-A loans, 9.3% were in foreclosure or REO and 4.8% were 90+ days past due (download data). Assuming that all of these end up in default and that the net recovery is zero, the total loss averages 21.3% between the Alt-A and subprime. The bulk of the RMBS were rated AAA, so they probably had about 10% subordination below them. Thus, assuming the securities sold to the NY Fed were evenly divided between Alt-A and subprime, the loss would be roughly (21.3%-10%)/90%, or 12.6%. This implies that a price of about 85% of par, or perhaps as low as 80% to allow a cushion, would have been a reasonable figure for the NY Fed to pay if the goal were to maximize the support of AIG while minimizing the loss to taxpayers. Instead, the NY Fed took advantage of the current dysfunction in the capital markets to buy the RMBS at a low price (for a scholarly article on how current market prices for mortgage-backed securities are below fundamental values, click here).

3 After the NY Fed loan is repaid, the first $1 billion (plus interest) of gains is paid to AIG subsidiaries, then the remainder is split 5/6 to the NY Fed and 1/6 to AIG subsidiaries.

4 Please see “Segment Information” on page 149 of AIG’s 2007 form 10-K for the operating income of AIG’s Life and Retirement Services businesses and aircraft leasing business.

(Disclosure: The author has no positions in AIG.)

| Copyright © 2008-2009 by John G. Appel. All rights reserved. You may link to any Content on this website. You may not republish, upload, post, transmit or distribute any Content without prior written permission. If you are interested in reprinting, republishing or distributing Content, please contact John Appel via the e-mail address shown on this website to obtain written consent. Modification of Content or use of Content for any purpose other than your own personal, noncommercial use is a violation of our copyright and other proprietary rights, and can subject you to legal liability. Disclaimer: This website is provided for informational purposes only. Nothing on this website is intended to provide personally tailored advice concerning the nature, potential, value or suitability of any particular security, portfolio or securities, transaction, investment strategy or other matter. You are solely responsible for any investment decisions that you make. Terms of Use: By using the site, you agree to abide by the Terms of Use, which includes further copyright information and disclaimers. |